June 2026 Monthly Second Helping: Highlighting Hot Topics in the Industry

What BBI Data Tells Us About Restaurant Traffic During the War’s Gas Price Surge

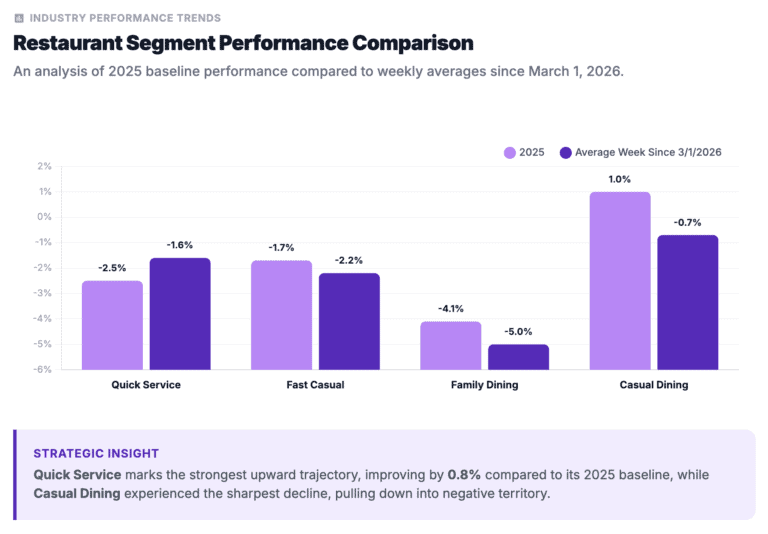

As gas prices have eased, Black Box Intelligence data reveals which restaurant segments proved most resilient during the recent price surge—and which felt the greatest impact.

Since the Memorandum of Understanding was signed by United States and Iranian leaders on June 17, gas prices have declined. National retail gas prices were $3.96 during the week ending June 29. That’s 67 cents lower than they were at the height of the conflict, but still 74 cents higher than the 2025 average.

A Black Box Intelligence study conducted during the early weeks of the conflict found that restaurant traffic growth has historically tended to decline when gas prices reach $3.50 per gallon. Now that the war is seemingly over (albeit precariously), we can look back to see how the restaurant industry performed.

Traffic Remained Resilient Despite Higher Gas Prices

Since early March, gas prices have been over $3.50 with most weeks well past $4.00 a gallon. However, the industry has been resilient. As of June 21, the weekly average since March 1 in terms of traffic growth for the industry was -1.9%. This is only -0.1 percentage points lower than same-store traffic growth for all of 2025. In other words, there has not been a significant downturn for restaurants.

These numbers since March have been held up by Upscale Casual, Casual Dining and Quick Service.

The Winners: Quick Service Was the Only Segment to Improve

While Upscale Casual performed the best during this timeframe, it is likely unrelated to the gas hikes. Black Box Intelligence found no correlation between gas prices and Upscale Casual traffic performance and it also had relatively easy laps compared to the same timeframe in 2025.

Quick Service was the only segment which seemed to benefit from the gas hikes. Although same-store traffic averaged -1.6% during these weeks, it was the only segment which saw improvement. It recorded 0.8% better traffic growth than 2025.

The Losers: Casual and Family Dining Lost Ground

Casual Dining actually performed well compared to the other segments during this time period, which helped to lift the Industry performance. However, compared to 2025 annual numbers, they actually saw a drop of -1.8 percentage points in their average same-store traffic growth.

While gas prices may have played a part in this slowdown, it’s likely multifactored, including that 2025 was a banner year for several large Casual Dining chains.

Although Fast Casual historically has the highest positive correlation with gas prices, it remained mostly flat compared to the rest of the year and was even -0.5 percentage points lower than 2025.

Family Dining, which unfortunately is a segment that had been struggling before the gas price hike, was hit hard by this latest challenge. Since 2017 (excluding COVID years) this segment has a very negative relationship with gas prices and the past few months were no exception. During the weeks since the war began, Family Dining averaged -5.0% traffic growth, nearly a percentage point lower than the previous year.

Delivery Saw the Greatest Impact

However, the biggest victim of the gas hikes in terms of the restaurant industry was delivery sales. Delivery sales have a negative correlation with gas prices historically. This is likely because as rising gas prices pressure consumers, they will naturally avoid the most expensive way to get food and some (not all) delivery channels have passed the added fuel costs onto the consumer.

Since March, delivery sales have fallen 4.6 percentage points below the 2025 average. Fast Casual experienced the largest decline, which may help explain why the segment did not see the same traffic benefit as Quick Service.

Unfortunately, even if hostilities have permanently ceased, the restaurant industry won’t fully understand the financial impact of the conflict for some time. Supply chain disruptions could continue pushing food costs higher for months—or even up to a year—before operators pass those increases on to an already price-sensitive consumer.

State of the Restaurant Industry Webinar Series

Want More Detail? Register for our Quarterly Deep Dives on the Restaurant Industry

Unrivaled Restaurant Financial Intelligence

Explore Daily Comp Sets With BBI