Monthly Restaurant Trends Review

Out of the Box: May 2026

-

Resilience Defies Pressure: Consumers continued dining out despite rising inflation and gas prices, driving 1.8% sales growth.

-

Tactical Trade-Offs: Sales accelerated while traffic softened, signaling consumers are spending more but visiting less often.

-

Affordability Under Fire: Family Dining remained the weakest segment as traffic declines and higher checks pressured value.

-

The Retention Plateau: Management turnover remained above 40%, making competitive compensation a critical retention tool.

Executive Insights: Sales Growth Accelerates as Consumers Trade Frequency for Check Size

In this Issue:

-

The Big Picture: May 2026 Sales and Traffic Trends

-

Segment Focus: Family Dining

-

Best vs Worst: Region and Segment

-

Staffing Review: Limited Service Restaurants, Management

May 2026 Restaurant Industry Trends

The Big Picture: Sales and Traffic Trends

May Restaurant Performance: Resilience Amidst Persistent Macroeconomic Friction

Consumers are navigating an increasingly complex economic environment, contending with the highest inflation rate in over two years and fuel prices that remained stubbornly above $4.45 per gallon throughout May. Yet, the data continues to point to a consumer who is adapting rather than retreating. Sales growth accelerated as diners prioritized dining out, even as they shifted to a strategy of trading visit frequency for higher per-visit spend.

By the Numbers: Sales Growth Accelerates Despite Traffic Pressure

May’s performance suggests consumers are managing economic pressure through selective spending rather than broad cutbacks. Diners aren’t abandoning restaurants; they are simply recalibrating their cadence. By accelerating sales while traffic softens, the data confirms that guests are protecting their dining-out habits by prioritizing check size over frequency.

-

Same-store traffic growth: Declined -2.0% in May, a modest 0.3 percentage point dip from April.

-

Same-store sales growth: Increased to 1.8% in May, accelerating from 1.5% in April and marking the industry’s strongest sales performance since early March.

The Silver Lining: A Gradual Slowdown, Not a Demand Shock

While traffic softened in May, the decline remained remarkably controlled given the broader economic backdrop. In fact, same-store traffic in May was stronger than in February and March—periods when inflationary and energy pressures were considerably lower. This indicates that while guests are becoming more selective, they have yet to initiate a broad or aggressive retreat from their restaurant budgets.

The Bottom Line: Rising costs are influencing how often consumers dine out, but not if they dine out. For now, the industry is navigating a gradual, manageable moderation in demand rather than a sharp, systemic shock.

| Month | Jun ’25 | July | Aug | Sep | Oct | Nov | Dec | Jan ’26 | Feb | Mar | Apr | May |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Comp. Sales | +2.0% | +2.4% | +2.3% | +1.1% | +0.7% | +0.0% | -1.0% | +1.0% | +1.6% | +0.7% | +1.5% | +1.8% |

| Comp. Traffic | -0.9% | +0.1% | -0.2% | -1.5% | -2.0% | -2.9% | -3.3% | -1.1% | -2.0% | -2.3% | -1.7% | -2.0% |

Note: These numbers have been modified slightly following a benchmark recalibration.

May 2026 Restaurant Segment Performance

Best vs Worst: Restaurant Industry Segment

Segment Performance: The “Affordable Luxury” Pivot

May’s segment data confirms that the economic squeeze is driving a significant recalibration in consumer behavior. While most segments maintained positive sales growth, the gap between performance leaders and laggards has widened, signaling a clear shift toward “affordable luxury.”

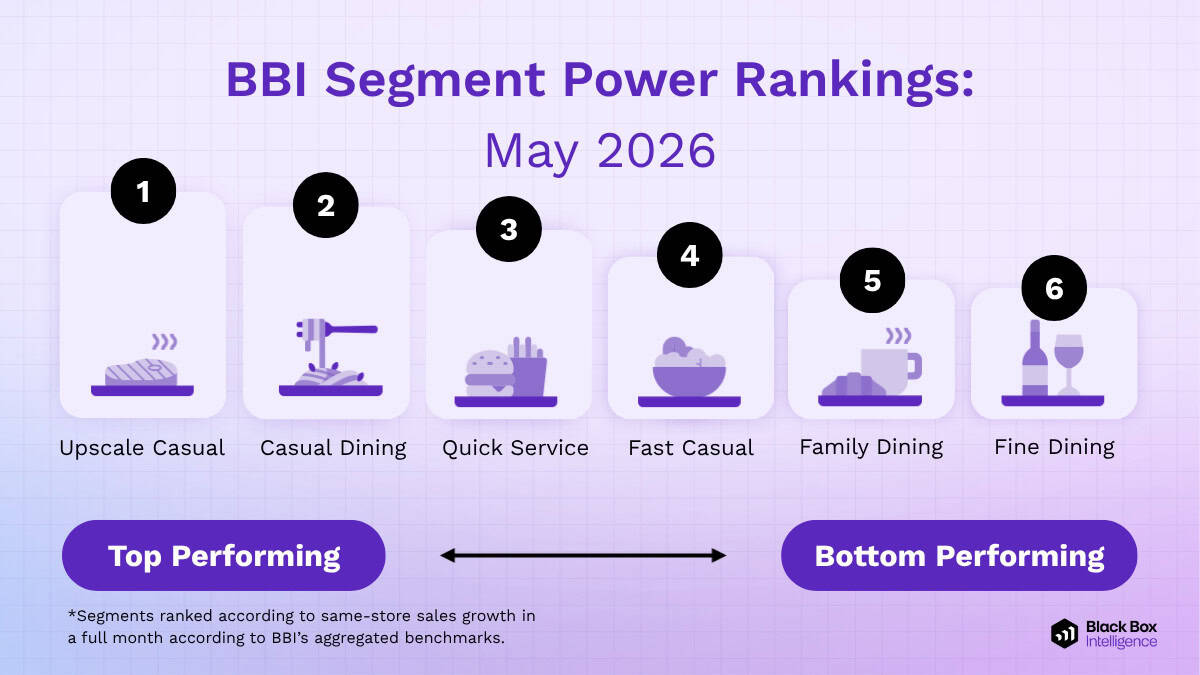

The High-End Bifurcation: Upscale Casual vs. Fine Dining

A fascinating dynamic has emerged over the last two months: the high end of the market has become the most polarized space in the industry.

-

Upscale Casual (The Winner): For the 2nd consecutive month, Upscale Casual claimed the top spot. It has effectively positioned itself as the go-to “affordable luxury” option for consumers feeling the weight of inflation.

-

Fine Dining (The Laggard): Conversely, Fine Dining continues to struggle as the worst-performing segment. This decline is likely twofold: mid-income diners are trading down from Fine Dining to more sensible Upscale Casual options, while broader economic uncertainty is tightening corporate dining budgets.

Growth Divergence: Acceleration vs. Deceleration

The industry’s performance in May was a story of two different trajectories compared to April:

-

Segments Accelerating: Upscale Casual, Casual Dining, and Fine Dining all saw their year-over-year growth rates accelerate in May.

-

Segments Decelerating: Quick Service, Fast Casual, and Family Dining experienced a deceleration in their growth rates, indicating that value-conscious segments are beginning to face stiffer headwinds.

May Restaurant Performance: Region Focus

Best vs Worst: Region

Regional Performance: Local Volatility Masks Nationwide Growth

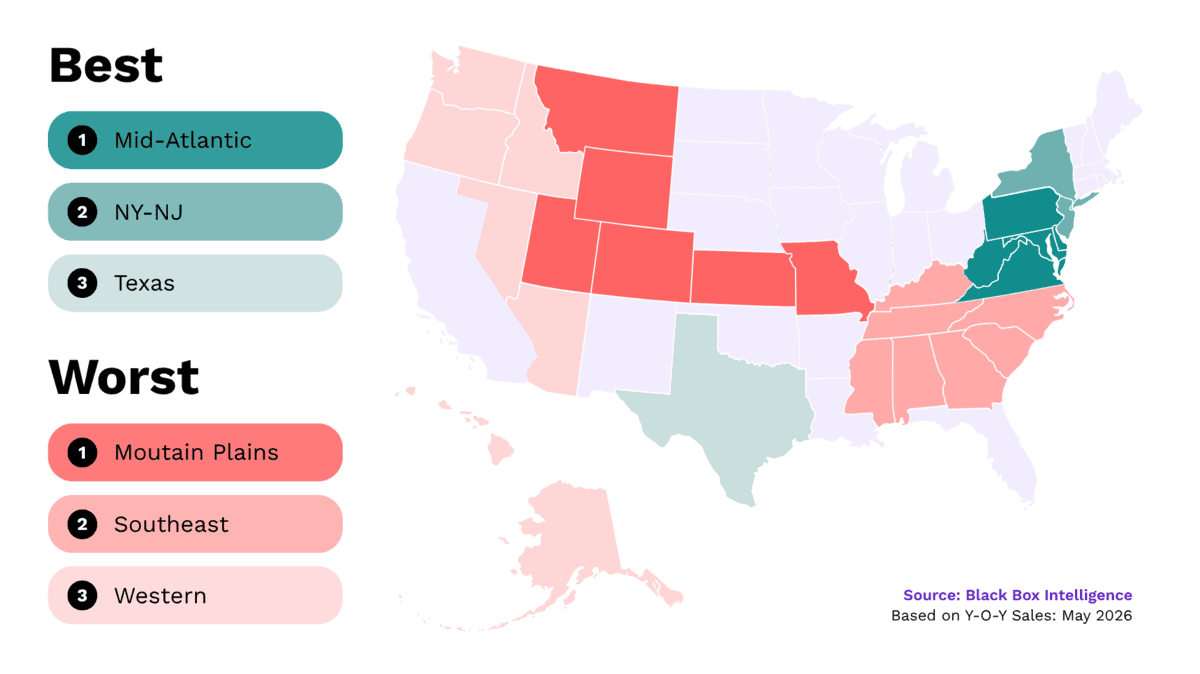

For the third consecutive month, every region nationwide achieved positive same-store sales growth. However, beneath this topline stability lies significant regional volatility. While most regions saw acceleration compared to April, four areas—Florida, the Southwest, California, and the Mountain Plains—bucked the trend, experiencing a softening in year-over-year sales growth.

The Mid-Atlantic Returns to the Top

The Mid-Atlantic reclaimed the title of top-performing region in May, driven by robust performance across Delaware, Maryland, Pennsylvania, Virginia, and West Virginia.

-

The Volatility Factor: Despite taking the top spot in both March and May, the region’s performance remains highly inconsistent—ranking 2nd-worst in February and 7th in April. This erratic trajectory suggests factors beyond underlying consumer demand, such as localized events or weather patterns, are heavily influencing the region’s month-to-month results.

Mountain Plains Faces Economic Headwinds

The Mountain Plains region ended May as the worst performer, showing a marked deterioration in its ranking since earlier this spring.

-

State-Level Pressure: Sales were dragged down by negative growth in Missouri and Montana, alongside flat year-over-year sales in Utah.

-

The Energy Link: States within the Mountain Plains have experienced some of the nation’s largest gas price increases since March, which may be adding pressure to discretionary spending in the region.

Restaurant Segment Deep Dive: May 2026

State of Restaurant Segment Performance: Family Dining

Family Dining: Caught Between Inflation and Affordability

Family Dining was the industry’s weakest-performing segment over the last three months, posting -0.9% same-store sales growth. Along with Fine Dining, it was one of only two segments to report negative sales growth during the period.

A Segment Under Pressure

The challenges are not new. Family Dining posted the weakest sales growth in 2025 and remains the only segment experiencing same-store sales contraction through the first five months of 2026. Ongoing traffic declines continue to weigh on performance.

When Check Growth Becomes a Headwind

Family Dining has recorded the strongest average check growth of any segment so far this year, extending a trend that has persisted for several years. While higher checks have supported sales, they may also be contributing to traffic losses as consumers become more price conscious.

Value Matters More Than Ever

As inflation continues to strain household budgets, many guests appear to be:

-

Trading down to lower-priced restaurant options

-

Reducing dining-out frequency

-

Becoming more selective about full-service occasions

Family Dining’s traditional value proposition is facing increased scrutiny from consumers looking to stretch every dollar.

The Bottom Line: Family Dining sits at the center of today’s affordability challenge. Restoring traffic growth will depend on convincing budget-conscious consumers that the full-service experience remains worth the premium.

State of Restaurant Workforce in 2026

Go Deep on the Latest Workforce Trends with Our Comprehensive Annual Research Study

Staffing, Workforce, And Employment Focus

Current Turnover Trends in Limited Service Restaurants

A New Retention Equilibrium

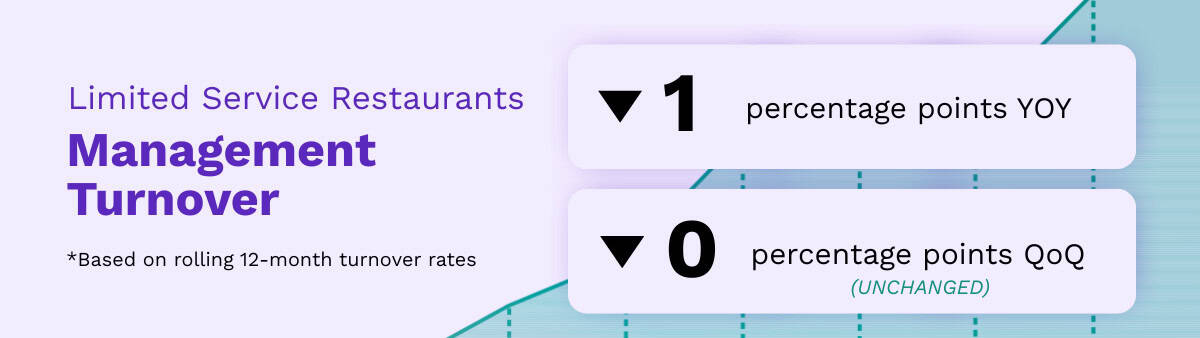

Management turnover in Limited Service restaurants remains below pre-pandemic norms, but recent gains have slowed considerably. As of April, rolling 12-month turnover rates declined by just 1 percentage point year-over-year and remained unchanged from Q1 2026.

While operators have made meaningful progress on retention in recent years, turnover remains above 40%, suggesting the industry may be approaching a new equilibrium where further gains are increasingly difficult to capture.

Compensation Remains the Strongest Retention Lever

According to the latest Black Box Intelligence operator survey, larger pay increases remain the most effective tool for reducing management turnover. Compensation also continues to be a common thread among the top reasons managers leave, whether for a promotion elsewhere or simply a higher-paying opportunity.

The Pay Gap Tells the Story

The data reveals a clear, actionable relationship between pay and retention. Our analysis of General Manager (GM) compensation shows a distinct divide:

-

The Stability Premium: The 25% of Limited Service companies with the lowest turnover pay GMs roughly $6,600 more than their local competitors.

-

The Attrition Penalty: By contrast, the 25% of companies with the highest turnover pay about $6,000 less than local peers.

The Bottom Line: The industry’s turnover problem has improved, but it hasn’t disappeared. As retention gains become harder to achieve, compensation remains one of the clearest differentiators between operators that successfully retain management talent and those that struggle to keep it.

Our Take on State of the Restaurant Industry in May 2026

BBI Says…

May’s results reinforced a theme that has defined much of 2026 so far: consumers remain remarkably resilient despite growing economic pressure. Higher gas prices and accelerating inflation have yet to trigger a significant pullback in restaurant spending, but the underlying economic signals suggest tougher conditions may be ahead.

“The biggest takeaway from May is that consumers are proving remarkably resilient despite mounting economic pressure. Restaurant spending has become a more ingrained part of everyday life than it was in previous cycles, which is helping the industry weather higher gas prices and accelerating inflation.

That said, we’re becoming increasingly cautious about the second half of the year. Inflation has accelerated significantly over the last three months, and there are signs that consumers may not have felt the full impact yet. As higher costs continue to move through the economy, households are likely to face even greater pressure on their budgets in the months ahead.

We don’t expect a crisis for the restaurant industry, but we do expect consumers to become more selective. Traffic will likely feel more pressure than sales as guests look to protect dining-out occasions by trading down, seeking value, and making tougher decisions about where they spend their discretionary dollars.”

The good news for operators is that consumers are adjusting their behavior rather than abandoning restaurant occasions altogether. The challenge will be maintaining traffic as value becomes increasingly important and additional inflationary pressures work their way through the economy. The second half of 2026 is likely to be defined not by a collapse in demand, but by a more selective consumer looking to stretch every dollar.

Victor Fernandez

Chief Insights Officer

Black Box Intelligence

State of Restaurant Industry

Quarterly Webinar Deepdives

We go into way more detail in our flagship quarterly State of the Industry (SOTI) webinar – our definitive take on the latest developments and a must attend for anyone in the restaurant industry.