Monthly Restaurant Trends Review

Out of the Box: April 2026

-

Comp Sales grew a muted 1.5% against a -1.7% drop in Comp Traffic, signaling a stark consumer pullback driven by sticky inflation.

-

Upscale Casual is feeling the squeeze of a K-shaped economy, forcing middle-income guests to accelerate trade-downs to value-driven segments.

-

Sharp divides between the best and worst regions highlight how sudden weather anomalies compound the pressure of rising regional gas prices.

-

Limited Service non-management retention finally stabilized, proving that aggressive, pandemic-era wage corrections are now insulating operators in a cooling job market.

Executive Insights: Traffic Drops as Trade-Downs Accelerate

In this Issue:

-

The Big Picture: April 2026 Sales and Traffic Trends

-

Segment Focus: Upscale Casual

-

Best vs Worst: Region and Segment

-

Staffing Review: Limited Service Restaurants, Non-Management

April 2026 Restaurant Industry Trends

The Big Picture: Sales and Traffic Trends

April Restaurant Performance: Consumer Resilience Defies Economic Headwinds

April delivered stronger-than-expected results for the restaurant industry. With the severe weather anomalies of the first quarter finally subsiding, a much clearer baseline for restaurant performance has emerged. The takeaway is undeniable: despite a decisively negative macroeconomic outlook, the consumer remains resilient and fiercely protective of their dining-out budgets.

The Gas Price Paradox: Traffic Improves Despite Breaking the $3.50 Threshold

Historical Black Box Intelligence analysis reveals a harsh industry reality: restaurant traffic historically declines once the national average for a gallon of regular gas surpasses $3.50. We are currently operating well above that tipping point, yet the consumer is pushing through the friction.

-

Gas prices broke the $3.50 threshold in the second week of March.

-

The national average has remained above $4.00 since the fourth week of March.

-

For three out of four weeks in April, average gas prices climbed to a punishing $4.25.

Despite these severe headwinds at the pump, restaurant same-store traffic growth actually improved throughout the month.

By the Numbers: Traffic Regains Ground as Sales Stabilize

Same-store performance tells a story of steady, incremental recovery. While February’s numbers were artificially propped up by highly favorable weather and easy laps over soft 2025 performance, April’s data proves that organic demand is holding steady.

-

Same-store traffic growth: Improved to -1.7% in April, up from -2.2% in March and -2.1% in February.

-

Same-store sales growth: Reached 1.5% in April, accelerating past March’s revised 1.4% and remaining highly competitive with February’s weather-aided 1.8%.

The Macro Buffer: Tax Refunds Fuel the Restaurant Wallet

If inflation and gas prices are draining consumer wallets, what is funding this continued restaurant spend? A major factor counteracting these inflationary pressures is a highly favorable 2026 tax season. A significant influx of capital from the IRS has provided consumers with the discretionary padding needed to absorb higher prices.

-

As of May 1, the IRS has issued 7 million more refunds than the prior year.

-

The average refund size is $326 larger in 2026.

The Bottom Line: Sky-high gas prices and persistent inflation haven’t broken the dining habit. Buffered by a lucrative 2026 tax season, consumers are absorbing macroeconomic friction to maintain their restaurant lifestyle, signaling that operators should focus heavily on capturing this protected spend before the tax-refund halo fades.

| Month | May ’25 | Jun | July | Aug | Sep | Oct | Nov | Dec | Jan ’26 | Feb | Mar | Apr |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Comp. Sales | +1.4% | +2.0% | +2.4% | +2.3% | +1.1% | +0.7% | +0.0% | -1.0% | +1.0% | +1.6% | +0.7% | +1.5% |

| Comp. Traffic | -1.0% | -0.9% | +0.1% | -0.2% | -1.5% | -2.0% | -2.9% | -3.3% | -1.1% | -2.0% | -2.3% | -1.7% |

Note: These numbers have been modified slightly following a benchmark recalibration.

April 2026 Restaurant Segment Performance

Best vs Worst: Restaurant Industry Segment

Segment Performance: The K-Shaped Economy Squeezes the Middle

A persistent theme in consumer spending is the “K-shaped” economy. While higher-income consumers have historically boosted spending, middle- and lower-income diners are aggressively trading down to more affordable options. This dynamic is creating a severe squeeze on brands caught in the middle, and April’s restaurant results mirrored this reality perfectly.

The top-performing segments for same-store sales growth occupied completely opposite ends of the dining and average-check spectrum: Upscale Casual and Quick Service.

-

Upscale Casual claimed the top performance spot in the industry for the first time in years, continuing a steady upward climb.

-

A one-time income boost from larger 2026 tax refunds likely fueled this surge, empowering consumers to trade up for special occasions, particularly around the Easter holiday.

Fine Dining Falters: Tech Layoffs and Corporate Cutbacks Drive the Trade-Down

Despite catering to the exact higher-income demographic that has historically driven the K-shaped recovery, Fine Dining was the worst-performing segment in April. The segment has now experienced two consecutive months of decline, suggesting a shift in affluent consumer behavior driven by several macroeconomic headwinds:

-

Corporate tightening: Economic pressures are forcing businesses to aggressively scale back on corporate dining and travel expenses.

-

White-collar layoffs: High-income earners, particularly in technology, are facing severe job insecurity. Over 100,000 tech industry workers lost their jobs in the first few months of 2026 alone.

-

The wealthy trade-down: Broader economic anxieties are prompting even insulated, wealthy diners to downgrade some of their premium dining occasions from Fine Dining to Upscale Casual.

The Bottom Line: The extremes of the industry are winning. As economic pressures force budget-conscious consumers into Quick Service and push anxious, wealthy diners down from Fine Dining into Upscale Casual, operators must clearly define their value proposition or risk getting crushed in the squeezed middle.

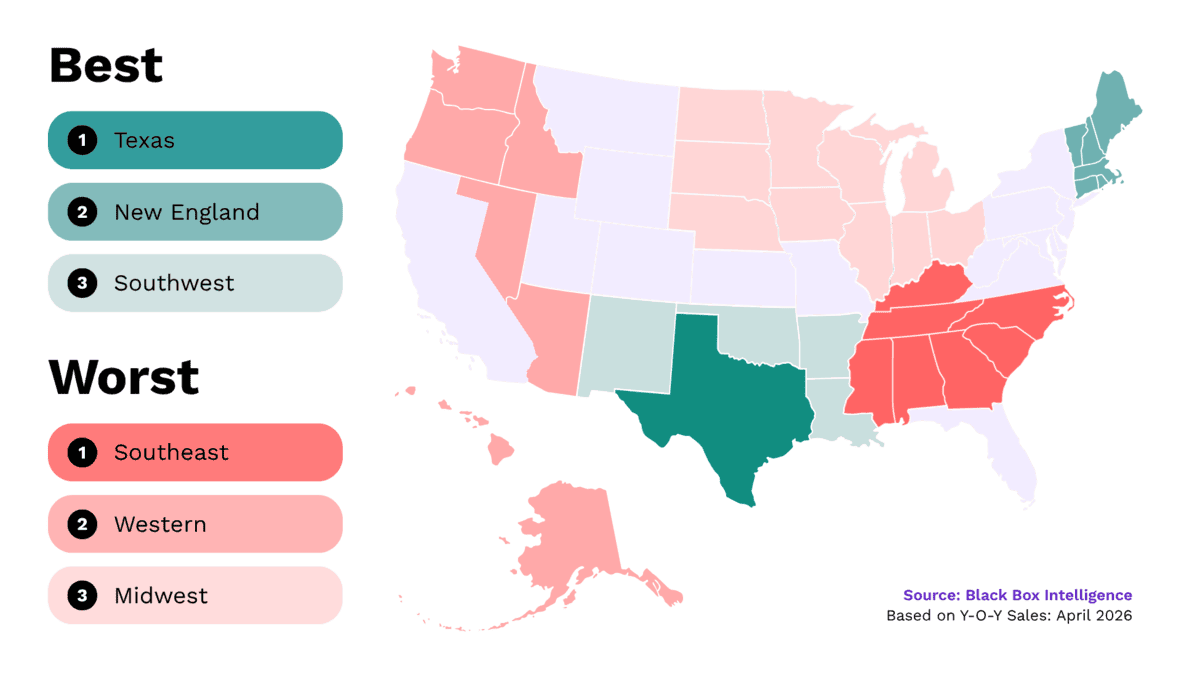

April Restaurant Performance: Region Focus

Best vs Worst: Region

Regional Performance: Nationwide Sales Growth Masks Localized Vulnerabilities

Despite the looming threat of inflation, April delivered a broadly positive month for the industry. Every region across the country posted positive same-store sales growth, with the vast majority accelerating their year-over-year rate compared to the previous month. However, this national resilience masked softening momentum in specific pockets of the country, primarily the Mid-Atlantic, Midwest, and Southeast.

The Southeast Squeeze: Energy Costs Disproportionately Hit Lower-Income Diners

The Southeast is experiencing a sustained three-month downturn, ranking as the absolute bottom performer in both February and April, and sitting in the bottom three during March. While February’s poor performance was largely a weather-driven mirage caused by severe winter events, the current decline is rooted in severe consumer softness.

-

The Southeast contains several states with the lowest average income levels in the nation.

-

Skyrocketing gas prices and persistent overall inflation represent an outsized hurdle for lower-income consumers whose finances are already heavily constrained.

-

Diners in this region are being forced to aggressively curb discretionary restaurant spending to absorb rising costs for everyday essentials.

Texas Takes the Top Spot: A Genuine Resurgence or an Easy Historical Lap?

In stark contrast, Texas claimed the title of best-performing region in April, continuing a steady climb in same-store sales rankings over recent months. While booming oil prices undoubtedly offer a localized economic boost to the state’s massive energy sector, context is critical when evaluating this apparent surge.

-

In today’s diversified economy, the broader Texas consumer base is still fighting the same high-energy-cost headwinds as the rest of the country.

-

April’s apparent strength is heavily aided by an exceptionally easy historical lap; exactly one year ago, Texas reported the third-weakest sales growth out of all eleven regions.

The Bottom Line: National top-line growth is holding strong, but regional realities are starkly divided by local economics. Operators in vulnerable, lower-income territories like the Southeast must prepare for a sustained pullback in dining frequency, while brands celebrating the Texas boom must carefully analyze how much of their success is driven by genuine organic demand versus the sheer benefit of weak prior-year data.

Restaurant Segment Deep Dive: April 2026

State of Restaurant Segment Performance: Upscale Casual

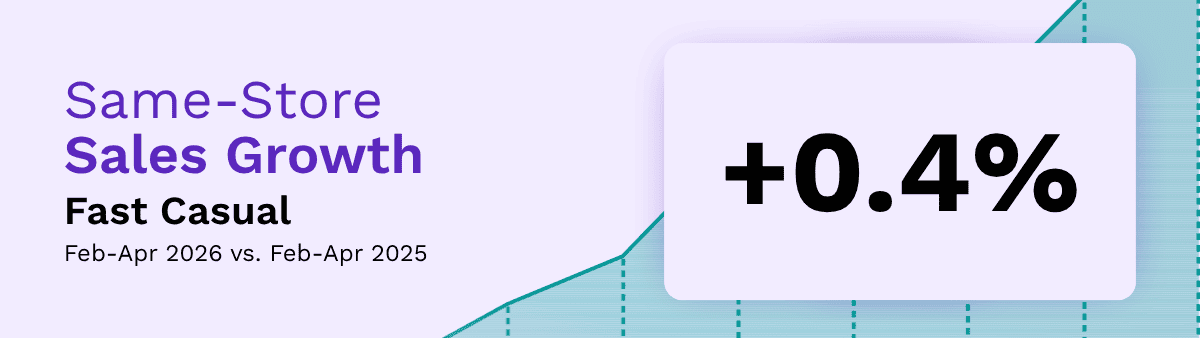

Fast Casual Under Fire: Losing the Value Battle on Two Fronts

Despite its traditional reputation as a budget-friendly limited-service option, Fast Casual performance has faltered in recent months. The segment is currently trapped in a brutal market-share battle, bleeding value-conscious guests to competitors on both sides of the dining spectrum.

-

Quick Service is successfully capturing the heavily strained consumer trading down for the absolute lowest cost.

-

Casual Dining chains are aggressively repositioning themselves, luring guests away by offering a superior full-service experience at a highly comparable price point.

The Tipping Penalty: Hidden Costs Erode Segment Appeal

Fast Casual’s low-cost positioning is being further compromised by the ubiquity of touchscreen tipping. When guests are strongly prompted to tip at the counter before receiving their meal or full service, the total out-of-pocket cost quickly bridges the gap between limited service and full service. This friction steadily erodes the segment’s perceived value advantage versus Casual Dining.

The resulting consumer pullback is clearly reflected in recent performance data.

-

Over the last three months, Fast Casual same-store sales growth has stagnated at a very weak 0.4%.

-

This sluggish performance severely lags the growth recorded by Casual Dining, Quick Service, and Upscale Casual during the exact same period.

The Bottom Line: Caught between the absolute affordability of Quick Service and the elevated experience of Casual Dining, Fast Casual is suffering a severe value-proposition crisis. To reverse this sluggish 0.4% growth trend, operators must aggressively defend their competitive advantage and ensure that hidden costs—like aggressive counter tipping—don’t accidentally price them out of the budget-friendly market.

State of Restaurant Workforce in 2026

Go Deep on the Latest Workforce Trends with Our Comprehensive Annual Research Study

Staffing, Workforce, And Employment Focus

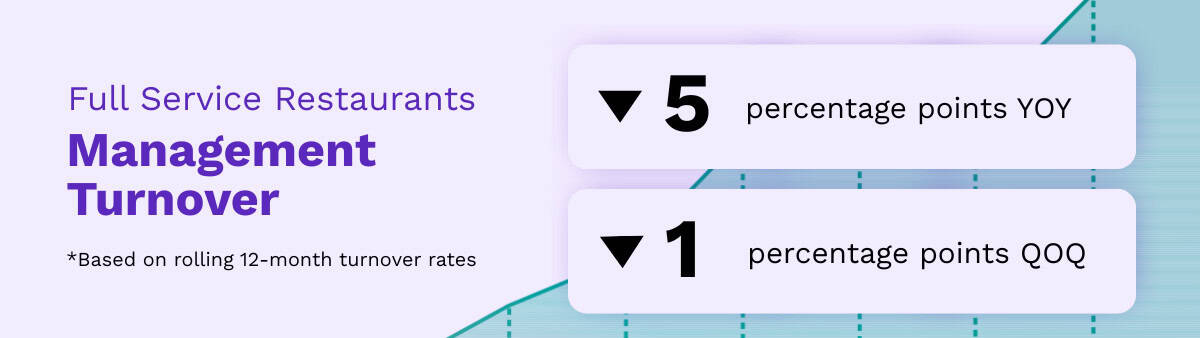

Current Turnover Trends in Limited Service Restaurants

The Silver Lining: A Cooling Labor Market Drives Historic Retention

While a hostile macroeconomic environment is actively suppressing consumer spending, it is quietly providing a massive operational tailwind: staffing stabilization. A steadily cooling labor market has driven restaurant turnover rates below those seen in recent quarters and years, allowing the industry to capitalize on stronger retention baselines than it experienced prior to the pandemic.

The GM Multiplier Effect: Tenured Leadership Drives Sales and Stability

While front-line staffing is improving, Black Box Intelligence data proves that retention at the management level is the ultimate operational differentiator. Tenured managers dictate the culture within the four walls of a restaurant, directly driving enhanced guest satisfaction through superior, consistent execution.

Looking at 2025 performance data, the financial and cultural ROI of retaining a General Manager is undeniable:

-

Restaurants that retained their General Manager for the entire year saw same-store sales and traffic growth outpace locations with manager attrition by 1.5 percentage points.

-

Locations with zero GM turnover experienced a massive 15 percentage point drop in hourly, non-management turnover compared to restaurants that lost leadership.

-

Keeping management in place acts as a direct anchor for team member engagement, proving that frontline stability starts at the top.

The Retention Playbook: How Top Brands Keep Their Leaders

If tenured leadership is the key to unlocking sales and traffic growth, how are top-performing brands keeping their managers from walking out the door? Black Box Intelligence data identifies a clear, proven correlation between lower manager turnover and aggressive total rewards strategies. The most successful operators are:

-

Paying base salaries that sit aggressively above the local market median.

-

Structuring higher, more lucrative target bonuses.

-

Absorbing the cost of care by paying a higher percentage of management health benefits.

-

Providing clear, actionable professional development opportunities.

The Bottom Line: A cooling labor market is a helpful tailwind, but true operational dominance requires a proactive investment in leadership. By funding highly competitive compensation and benefits packages for General Managers, operators trigger a multiplier effect that violently reduces costly frontline turnover and directly accelerates top-line growth.

Our Take on State of the Restaurant Industry in April 2026

BBI Says…

While March and April demonstrated consumer resilience, leading indicators signal a rapid slowdown. The University of Michigan’s Consumer Sentiment Index recently plummeted to a record low, driven by crushing inflationary anxieties.

Simultaneously, regular gas spiked to $4.63 by mid-May. Barring mid-2022 anomalies, prices have never been higher. The full inflationary impact hasn’t hit wallets yet, but it will aggressively squeeze low- and middle-income demographics in the coming months.

First-quarter restaurant strength was artificially propped up by temporary economic boosters that are now fading:

-

Highly favorable weather comparisons against a weak prior year.

-

Over 5 million more taxpayers receiving early refunds.

-

An average tax refund increase of $340.

-

A stock market-driven “wealth effect” among participating consumers.

The Bottom Line: An industry spending slowdown is imminent as record inflation and skyrocketing gas prices break consumer resilience. However, as squeezed diners actively hunt for value, operators in Quick Service and Fast Casual are perfectly positioned to capture this traded-down traffic and win market share.

Victor Fernandez

Chief Insights Officer

Black Box Intelligence

State of Restaurant Industry

Quarterly Webinar Deepdives

We go into way more detail in our flagship quarterly State of the Industry (SOTI) webinar – our definitive take on the latest developments and a must attend for anyone in the restaurant industry.