Monthly Restaurant Trends Review

Out of the Box: February 2026

-

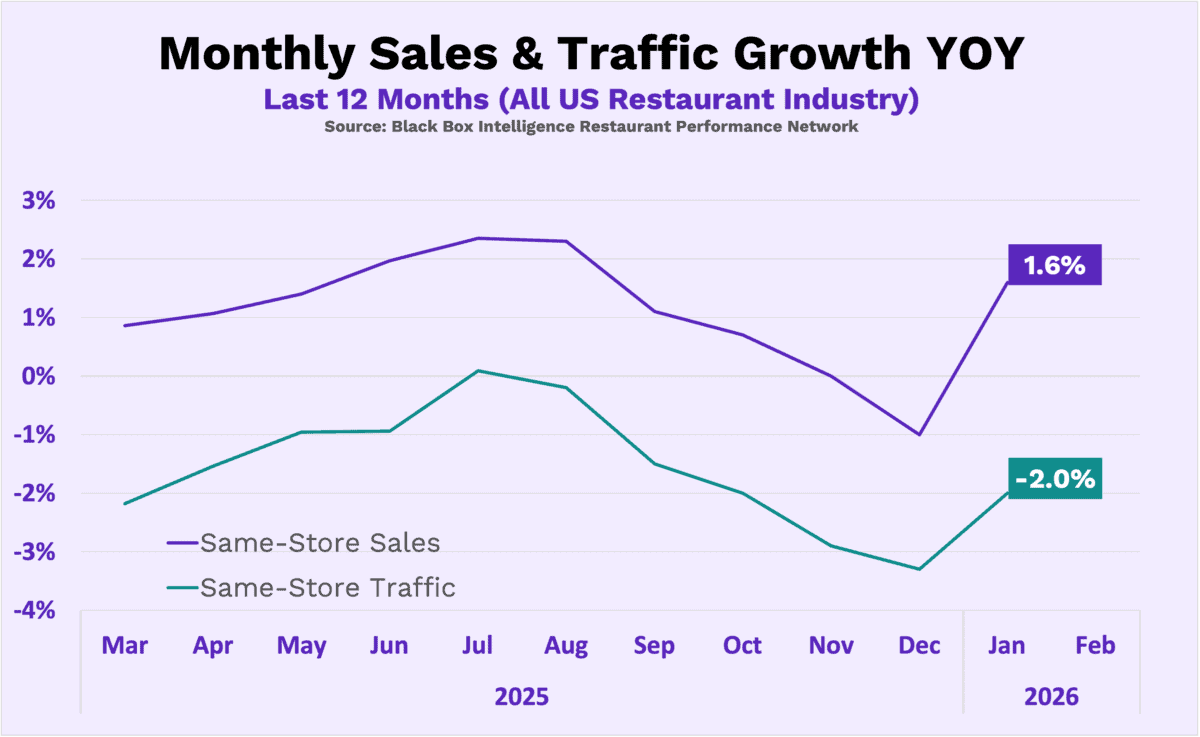

February sales rebounded to 1.6%, marking the industry’s strongest year-over-year performance since last August.

-

Favorable weather and easier year-over-year comparisons provided a significant sequential boost to monthly growth.

-

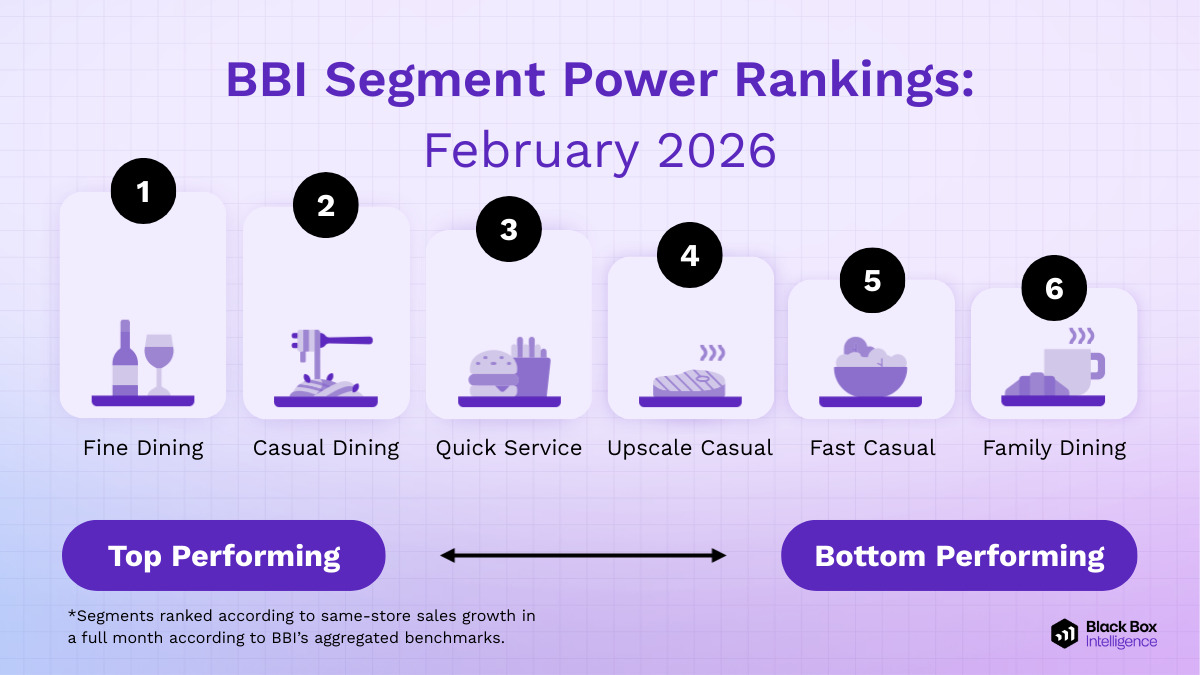

Fine Dining maintains its dominant lead, while Quick Service gains momentum from value-seeking consumers.

-

Improving workforce stability is driving better operational execution and a steady rise in guest sentiment.

-

Shifting macro conditions are accelerating the consumer trade-down, creating clear opportunities for value-led segments.

In This Issue:

-

The Big Picture: February 2026 Sales and Traffic Trends

-

Segment Focus: Quick Service

-

Best vs Worst: Region and Segment

-

Staffing Review: Full Service Restaurants, Non-Management

February 2026 Restaurant Industry Trends

The Big Picture: Sales and Traffic Trends

February Industry Performance: An “Easy Lap” Mirage?

February’s top-line numbers suggest a solid rebound for the restaurant industry, but the underlying data reveals a fragile recovery. While sales and traffic improved sequentially compared to the year-end slump, much of this growth is an artificial byproduct of “easy laps” against a weather-crippled February 2025.

Sales Growth: Context Matters

On the surface, February’s 1.6% same-store sales growth was the industry’s best performance since August. However, looking at the two-year stacked growth paints a different picture:

-

The 2025 Baseline: February 2025 saw a -2.5% decline, the weakest monthly growth in two years.

-

The 2-Year Reality: February 2026’s two-year stacked growth rate is actually negative at -0.2%.

-

Historical Context: This is only the second time in the last 12 months that the two-year sales stack has dipped into negative territory.

Traffic and Average Check Dynamics

Sales growth was propped up by a sharp acceleration in average check growth. In contrast, the traffic story remains concerning:

-

Softening Momentum: Same-store traffic growth actually worsened in February compared to the previous month.

-

Missed Tailwinds: Despite warmer weather in late February and higher-than-average tax refunds putting more cash in consumers’ pockets, traffic growth was the third weakest in the last 12 months.

-

A 12-Month Low: The two-year stacked traffic growth was -7.1%, the lowest mark seen in the last year.

The Bottom Line: February’s performance is not a sign of a robust consumer. When you strip away the favorable weather and the historically weak prior-year comparisons, the industry is struggling to regain true traffic momentum.

| Month | Mar ’25 | Apr | May | Jun | July | Aug | Sep | Oct | Nov | Dec | Jan ’26 | Feb |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Comp. Sales | +0.9% | +1.1% | +1.4% | +2.0% | +2.4% | +2.3% | +1.1% | +0.7% | +0.0% | -1.0% | +1.0% | +1.6% |

| Comp. Traffic | -2.2% | -1.5% | -1.0% | -0.9% | +0.1% | -0.2% | -1.5% | -2.0% | -2.9% | -3.3% | -1.1% | -2.0% |

Zooming Out: The Last 12 Months

The industry’s 12-month trajectory reflects a journey from artificial peaks to a weather-driven “mirage” recovery in early 2026. The mid-year surge, peaking in July and August 2025, was largely a product of favorable laps against soft 2024 data and a temporary boost from high-end consumer spending.

This momentum evaporated in Q4, bottoming out in December as an unfavorable holiday calendar shift combined with cooling consumer sentiment to drive traffic to a period low of -3.3%.

While the current rebound to 1.6% sales growth in February 2026 appears robust on the chart, it remains an atmospheric anomaly; the industry is currently benefiting from exceptionally warm weeks and “easy laps” against a storm-crippled February 2025, masking the fact that underlying two-year stacked traffic has actually hit a 12-month low.

February 2026 Restaurant Segment Performance

Best vs Worst: Restaurant Industry Segment

Segment Performance: The K-Shaped Reality Continues

February saw a near-universal improvement in same-store sales growth across all segments, with Quick Service as the lone exception. However, this rebound is largely an artifact of “easy laps” against a weak February 2025. The two-year stacked view reveals a more selective recovery: only Fine Dining and Casual Dining maintained positive growth compared to 2024 levels.

Fine Dining Leads the K-Shaped Recovery

Fine Dining continues its dominant streak, ranking as the top-performing segment in four of the last five months. This sustained strength supports the “K-shaped economy” thesis—high-income households remain the primary engine of restaurant consumption, effectively insulating premium segments from the volatility affecting the rest of the industry.

Family Dining and the Trade-Down Pressure

At the opposite end of the spectrum, Family Dining remains the industry’s bottom performer for the fifth consecutive month. As the Full Service segment with the lowest average check, it is most exposed to the economic pressures facing lower- and modest-income consumers.

The Bottom Line: These guests are increasingly opting for “trade-downs” to Limited Service restaurants. This migration is occurring at a significantly faster pace for Family Dining than for its Full-Service peers, as consumers prioritize value and convenience over the traditional sit-down experience.

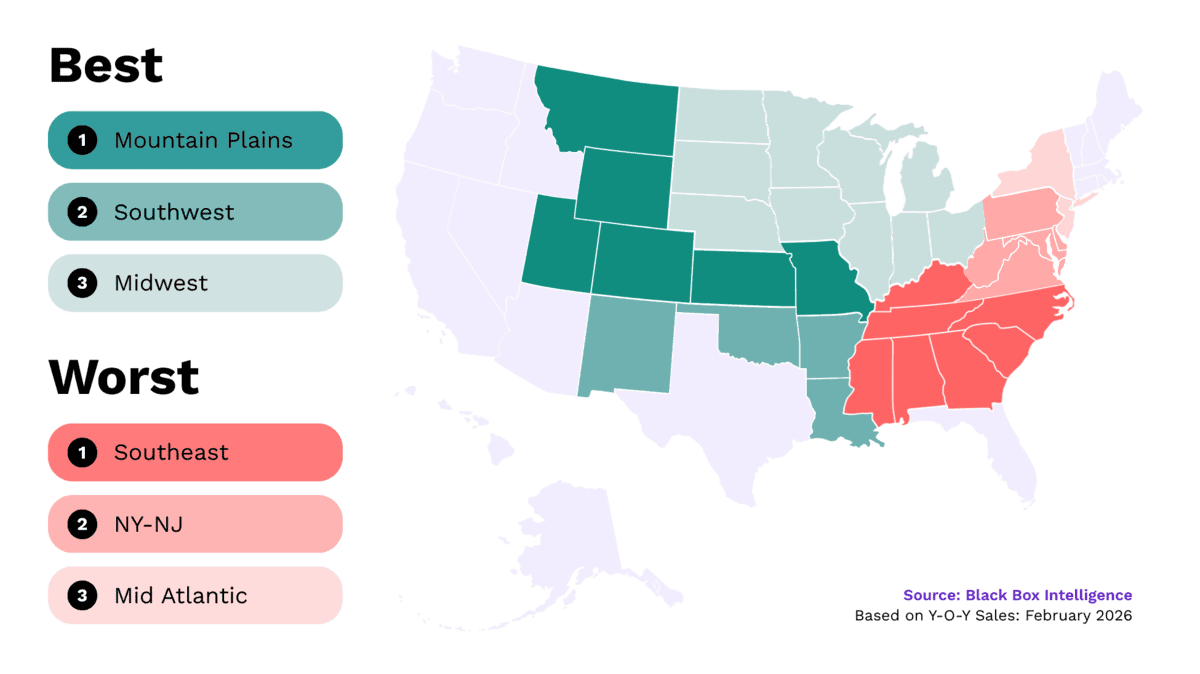

February Restaurant Performance: Region Focus

Best vs Worst: Region

Regional Performance: Weather remains the Primary Performance Engine

February saw widespread sales strength across the U.S., with nearly every region posting positive same-store sales growth. However, two notable exceptions—the Southeast and New York-New Jersey—failed to reach positive territory, highlighting how localized weather patterns continue to dictate monthly winners and losers.

Mountain Plains: The National Leader

For the second consecutive month (and the third time since November), the Mountain Plains topped the industry in sales growth.

-

The Weather Advantage: This sustained outperformance is directly linked to favorable conditions. The region experienced warmer temperatures in six of the last eight weeks compared to the same period in 2025.

The Southeast: A Localized Chill

The Southeast ranked as the weakest region in February, a departure from its typical “middle of the pack” performance seen throughout 2025.

-

Cold Front Headwinds: Unlike the rest of the country, the Southeast faced harsher relative temperatures during the first three weeks of February.

-

Performance Softening: This regional downturn follows a similar softening of sales growth previously observed in October and November.

The Bottom Line: Outside of the Mountain Plains’ weather-assisted surge, the failure of the Southeast and New York-New Jersey to achieve positive growth underscores the fragility of the current rebound. When favorable weather is removed from the equation, regional performance remains inconsistent.

Restaurant Segment Deep Dive: February 2026

State of Restaurant Segment Performance: Quick Service

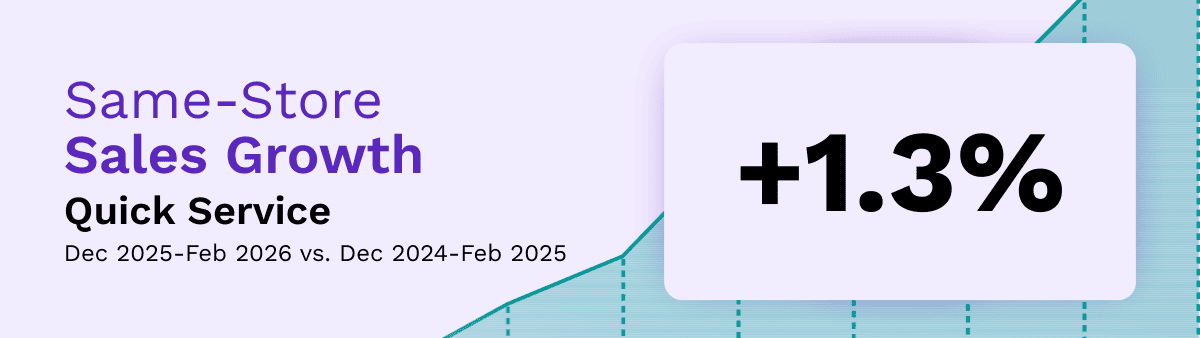

Quick Service: The Primary Beneficiary of the Accelerating Trade-Down

Since December, Quick Service (QSR) has solidified its position as the industry’s #2 performer in same-store sales growth, trailing only Fine Dining. While QSR was the second-strongest segment of 2025, it lagged significantly behind the then-dominant Casual Dining. That dynamic is now shifting as the economic environment cools.

The Inflationary Tailwinds for QSR

In an era of looming inflation and cautious consumer sentiment, the segment with the lowest average check naturally rises to the top. QSR’s value-driven brand identity is currently its greatest competitive advantage, offering a safe harbor for guests looking to manage their discretionary spending.

2026 Outlook: Protecting the “Dining Occasion”

We expect QSR to outperform most other segments throughout 2026. Two primary factors are driving this forecast:

-

Rising Gas Prices: Sharp increases at the pump typically serve as a catalyst for immediate shifts in restaurant spending.

-

Preserving Occasions: While some guests may reduce their total frequency, many are choosing to protect their “dining occasions” by trading down from Full Service to more budget-friendly QSR options.

The Bottom Line: QSR’s low-cost business model and emphasis on value make it uniquely positioned to capture the migration of guests away from higher-priced segments. As economic hardships persist, the trade-down to Quick Service isn’t just a trend—it’s a consumer survival strategy.

State of Restaurant Workforce in 2026

Go Deep on the Latest Workforce Trends with Our Comprehensive Annual Research Study

Staffing, Workforce, And Employment Focus

Current Turnover Trends in Full Service Restaurants

The Retention Dividend

A cooling labor market continues to provide a rare tailwind for the restaurant industry. The staffing volatility of the last few years has subsided, with turnover rates now trending lower than pre-pandemic benchmarks.

Full Service Stabilization

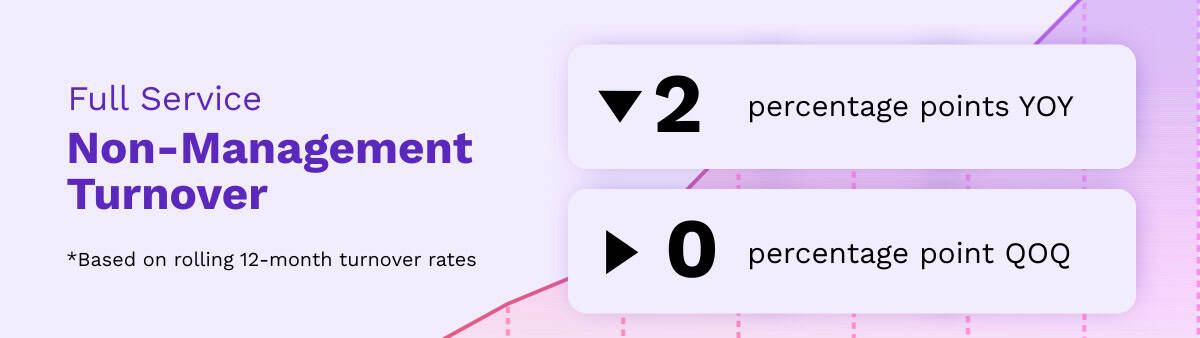

The stabilization of the restaurant workforce has gained significant momentum. As of January, the rolling 12-month turnover for non-management employees in Full Service restaurants was 2 percentage points lower than in Q1 2025. Crucially, these rates are now solidly below 2019 levels, signaling a definitive return to operational consistency after years of disruption.

The Financial and Operational Impact

This retention surge offers two primary benefits to operators:

-

Direct Cost Savings: Black Box Intelligence data shows that replacing a single hourly, non-management employee costs over $2,700. Sustained retention is now a primary lever for protecting unit-level margins.

-

The “Sentiment Loop”: Higher team tenure leads to superior execution. This is directly reflected in current upward trends in guest sentiment across food, service, and value metrics.

2026 Outlook: A New Labor Reality

As unemployment is projected to creep upward throughout the year, restaurant retention is expected to remain uncharacteristically strong compared to historical norms.

The Bottom Line: With turnover costs down and guest sentiment up, 2026 is the year for operators to shift their focus from “filling seats” to “optimizing execution.” Stable teams are no longer just an HR win; they are a prerequisite for driving traffic in a softening economy.

Our Take on State of the Restaurant Industry in February 2026

BBI Says…

“Data from the first two months of the year has been exceptionally noisy, characterized by significant tailwinds that mask the underlying fragility of the industry. January benefited from favorable weather, and February offered historically weak laps against the extreme winter conditions of 2025. While the IRS reported an 11% increase in average tax refunds as of March 6th, this translates to just $352 in extra spending power—far below the $1,000 originally estimated. With consumer debt at record highs and multiple categories competing for those limited dollars, restaurants will likely see only a small, temporary boost from this capital.

“The year was already poised to be challenging given high inflation expectations and a softening labor market, but new pressures are intensifying the situation. Gas prices have reached multi-year highs, and the University of Michigan’s Consumer Sentiment Index has hit its lowest point in over three years as conflict in the Middle East introduces further uncertainty. Our analysis shows that when gas prices spike, Limited Service segments like Fast Casual and Quick Service benefit most as trade-downs accelerate from guests wanting to protect their dining-out occasions. Those segments most vulnerable to these hikes are Family and Casual Dining. These disruptions strengthen our thesis that Fast Casual brands remain the best positioned to endure the year’s softening conditions.”

Victor Fernandez

Chief Insights Officer

Black Box Intelligence

State of Restaurant Industry

Quarterly Webinar Deepdives

We go into way more detail in our flagship quarterly State of the Industry (SOTI) webinar – our definitive take on the latest developments and a must attend for anyone in the restaurant industry.