Monthly Restaurant Trends Review

Out of the Box: December 2025

-

Sustained Growth Deceleration: December’s -1.0% sales and -3.3% traffic marked five months of slowing growth, signaling a downward trajectory heading into 2026.

-

K-Shaped Economy Trend Reflected in Segment Numbers: Fine Dining outperformed the industry—driven by high-income resilience and holiday splurging. Limited Service also posted stronger relative numbers, highlighting low income focus on cost.

-

Climate-Driven Volatility: Milder regions like Texas and California accelerated in December, while winter storms drove sharp performance declines across the Northeast and Midwest.

In This Issue:

-

The Big Picture: December Sales and Traffic Trends

-

Segment Focus: Fine Dining

-

Best vs Worst: Region and Segment

-

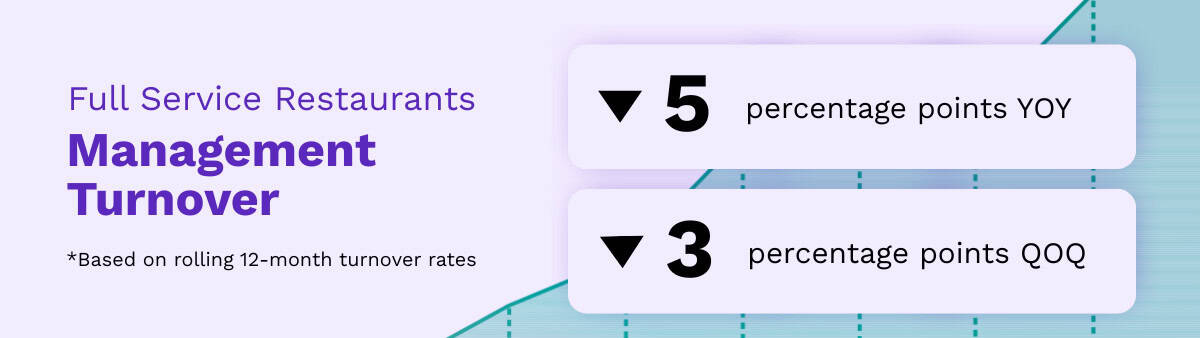

Staffing Review: Full Service, Management Turnover

December 2025 Restaurant Industry Trends

The Big Picture: Sales and Traffic Trends

Sustained Deceleration in Restaurant Demand

A softening labor market and persistent inflation are cooling restaurant demand despite early-year resilience. December marked the fifth consecutive month of decelerating year-over-year same-store sales and traffic, with growth turning negative for the first time in ten months. Excluding February’s weather-driven volatility, December represents the weakest performance since July 2024.

December Metrics and Year-End Trajectory

Specifically, December same-store sales growth hit -1.0%, a 1.0 percentage point deceleration from November. Same-store traffic growth dropped to -3.3%, down 0.4 percentage points month-over-month.

While 2025 was stronger overall than 2024—with sales up 0.9% compared to the previous year’s -0.2% and traffic improving to -1.9% from -2.8%—the trajectory is shifting. The momentum from a successful first half has faded, leaving the industry on a clear downward trend heading into 2026.

| Month | Jan | Feb | Mar. | Apr | May | Jun | July | Aug | Sep | Oct | Nov | Dec |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Comp. Sales | +2.5% | -2.5% | +0.9% | +1.1% | +1.4% | +2.0% | +2.4% | +2.3% | +1.1% | +0.7% | +0.0% | -1.0% |

| Comp. Traffic | -1.3% | -5.7% | -2.2% | -1.5% | -1.0% | -0.9% | +0.1% | -0.2% | -1.5% | -2.0% | -2.9% | -3.3% |

December 2025 Restaurant Segment Performance

Best vs Worst: Restaurant Industry Segment

High-Income Resilience and the Fine Dining Rebound

Fine Dining, Fast Casual, and Quick Service emerged as the top-performing segments in December. Fine Dining, in particular, saw a significant resurgence after trailing the industry from May through September. The segment claimed the top spot for sales growth in both October and December and ranked second in November.

This rebound reflects the 2025 “K-shaped” economic narrative, where high-income consumers fueled topline resilience.

Pent-up demand likely accelerated in the fourth quarter as consumer optimism improved; McKinsey & Company data supports this, noting that higher-income households were more likely to splurge in Q4 than in Q3.

Pricing Pressure and Family Dining Underperformance

Conversely, Family Dining recorded the weakest same-store sales growth for the third consecutive month. This underperformance is largely driven by aggressive pricing; the segment’s average check grew 3.4% year-over-year in December—the highest in the industry and nearly a full percentage point above the 2.5% industry average.

For lower- and middle-income guests squeezed by inflation, these elevated costs are likely a primary factor in skipping visits.

December Restaurant Performance: Region Focus

Best vs Worst: Region

Climate-Driven Regional Acceleration

December’s weakness was felt nationwide, with every region posting negative same-store sales. However, performance diverged sharply along climate lines. Regions with milder climates—specifically Texas, the West, and California—emerged as the top performers. While their growth remained negative, these regions saw an acceleration compared to November. This marks a significant shift, as all three had ranked in the bottom half of the industry for the previous eight months.

Winter Impact on High-Performing Markets

In contrast, regions prone to harsher winter conditions experienced the sharpest performance swings. New York-New Jersey, New England, and the Midwest transitioned from the top half of performers in November to the bottom in December. While local economic factors and market competitiveness play a role, year-over-year weather comparisons remain the primary driver of these regional results during the winter months.

Restaurant Segment Deep Dive: November 2025

State of Restaurant Segment Performance: Fine Dining

Despite these headwinds, the segment saw a late-year lift from resilient high-income spending and holiday “splurge” visits from typically budget-conscious guests. As a result, Fine Dining outperformed most other Full Service segments and more than half of the individual brands tracked within Casual Dining.

Staffing, Workforce, And Employment Focus

Current Turnover Trends in Limited Service Restaurants

Full Service operators saw a significant breakthrough in Q4 2025 as management turnover finally returned to pre-pandemic levels. This stability is a critical lead indicator for performance; Black Box Intelligence analysis reveals that lower management turnover correlates with improved hourly staff retention and higher guest sentiment, which ultimately drives traffic and sales growth.

The Bottom-Line Impact of Labor Stability

Reduced turnover also provides direct relief to the bottom line by curbing operational costs. In 2025, the hard costs associated with replacing a single General Manager—including separation, recruitment, and training—exceeded $17,500, while other management roles cost approximately $12,000 per replacement. Furthermore, falling turnover signals a cooling labor market, easing the wage pressure that has historically compounded the challenges of high food inflation.

State of Restaurant Workforce in 2025

Go Deep on the Latest Workforce Trends with Our Comprehensive Annual Research Study

Our Take on State of the Restaurant Industry in November 2025

BBI Says…

“Macroeconomic signals remain mixed. While Q3 GDP was strong and January sentiment improved for the second consecutive month, overall sentiment remains near historic lows. Rising unemployment throughout the second half of 2025 and persistent inflation—with tariffs presenting a recurring future threat—continue to weigh on the outlook.

“A primary concern for the industry is the accelerating cost of food. Restaurant price inflation reached 4.1% in December, the highest level since July 2024. Furthermore, the inflation gap between restaurants and grocery stores widened to an average of 1.7 percentage points over the last two months, up from 1.1 points in August and September. This increasing price disparity is intensifying consumer sticker shock and straining restaurant budgets.

“The industry enters 2026 on a clear downward trajectory, and this softness is likely to persist. While winter weather may cause short-term data fluctuations in the coming months, underlying economic headwinds suggest more cautious consumer spending ahead.”

State of Restaurant Industry

Quarterly Webinar Deepdives

We go into way more detail in our flagship quarterly State of the Industry (SOTI) webinar – our definitive take on the latest developments and a must attend for anyone in the restaurant industry.