Monthly Restaurant Trends Review

Out of the Box: September 2025

-

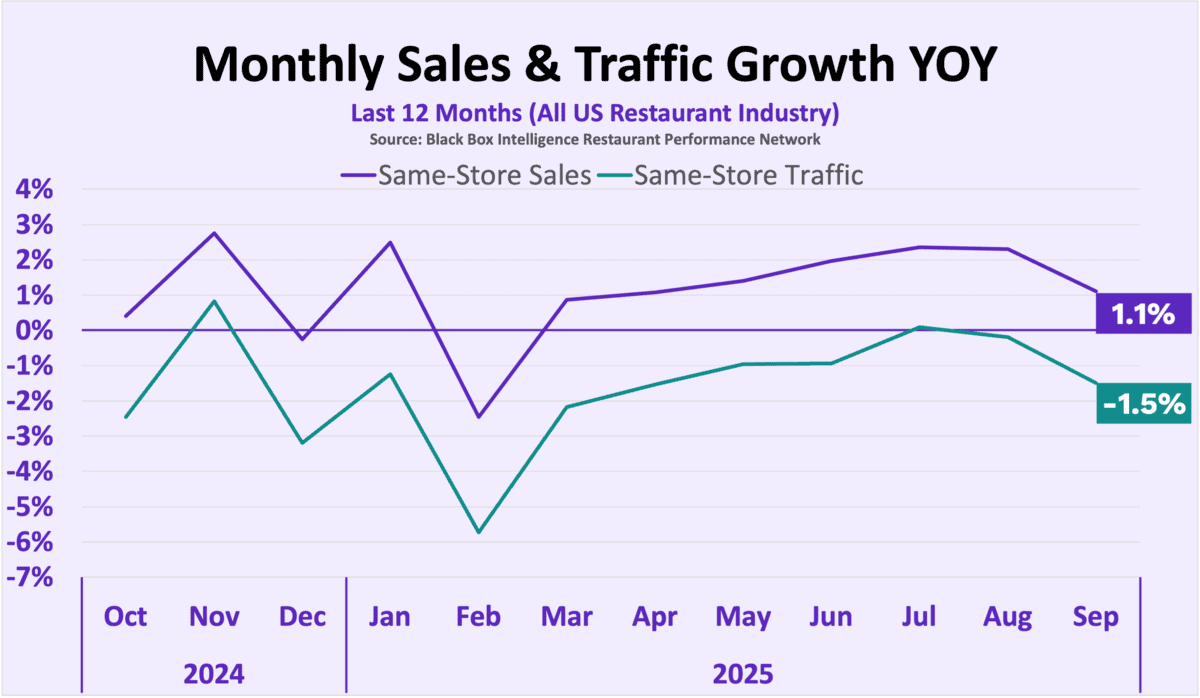

September comps: same-store sales +1.1% YoY; traffic -1.5%—weakest since April and the second straight monthly slowdown.

-

Segments: only 2 of 6 grew; Casual Dining still leads since March, but just 39% of brands were positive (median +3% vs -5% for decliners).

-

Regions: California and the West turned negative; Florida led again on easier comps, followed by the Southwest and Midwest.

-

Signals & outlook: Upscale Casual traffic -2.9% (Jul–Sep); retaining a GM correlates with +2 pp stronger traffic; QSR/Fast Casual best positioned as value/affordability drive choices.

In This Issue:

-

The Big Picture: September Sales and Traffic Trends

-

Segment Focus: Fast Casual

-

Best vs Worst: Region and Segment

-

Staffing Review: QSR Management Turnover

September 2025 Restaurant Industry Trends

The Big Picture: Sales and Traffic Trends

The headline for September: after a period that gave cause for optimism for restaurants, the weakening economy is – sadly – starting to show up in the numbers we’re seeing in our BBI Restaurant Performance Index.

In September, year-over-year same-store sales and traffic worsened for the second straight month, underscoring that the economy—and restaurant performance—are losing steam in the back half of the year.

After five months of improvement starting in March, the industry has now posted two consecutive months of lower YoY growth. Same-store sales rose 1.1% in September, 120 bps (basis points) below August’s pace, while same-store traffic fell to -1.5%, 130 bps (basis points) softer than last month—both the weakest results since April.

| Month | Oct. ’24 | Nov. ’24 | Dec. ’24 | Jan. | Feb. | Mar. | Apr. | May | Jun. | July | Aug | Sep |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Comp. Sales | +0.5% | +2.8% | -0.3% | +2.5% | -2.5% | +0.9% | +1.1% | +1.4% | +2.0% | +2.4% | +2.3% | +1.1% |

| Comp. Traffic | -2.5% | +0.9% | -3.2% | -1.3% | -5.7% | -2.2% | -1.5% | -1.0% | -0.9% | +0.1% | -0.2% | -1.5% |

September 2025 Restaurant Segment Performance

Best vs Worst: Restaurant Industry Segment

Only two of six segments grew same-store sales in September. For the prior two months, Upscale Casual and Fine Dining were the only segments in negative YoY sales, but September added Family Dining and Fast Casual to the decliners.

The high end continues to struggle as consumers trade down to more budget-friendly options. Even though higher-income guests are holding up better than lower-income cohorts, mounting uncertainty and worsening near-term expectations appear to be shifting some of their dining choices. Business expense cuts likely compound the drag. Fine Dining has been the worst performer on same-store sales growth for five straight months.

Meanwhile, Casual Dining kept the top spot in September, leading the industry in same-store sales growth every month since March—and by a wide margin. Many Americans seem to have rediscovered select Casual Dining brands, fueling gains and helping the segment take share.

But the wins aren’t universal. Only 39% of tracked Casual Dining companies posted positive same-store sales in September. Among the growers, median sales growth was about +3%, while brands in decline saw a median of -5%.

As we reported last month, QSR is showing some encouraging signs of recovery. That is definitely one to watch. (Some of) Casual Dining has stolen a march with strong value plays but if QSR can follow suit, a weakening economy and declining consumer confidence may play into that segment’s hands.

September Restaurant Performance: Region Focus

Best vs Worst: Region

Restaurant Segment Deep Dive: September 2025

State of Restaurant Segment Performance: Upscale Casual

Upscale Casual has stumbled through 2024 and 2025. After ranking second in same-store traffic growth in 2023, the segment has slipped into the bottom half of industry performers on traffic since then.

From July through September 2025, Upscale Casual traffic fell 2.9% on a same-store basis—outperforming only Family Dining and Fine Dining, the two weakest segments over that period.

Economic headwinds likely play a role. Years of high inflation have dampened consumer sentiment, while tariff chatter—and its potential inflationary impact—has darkened near-term expectations. These pressures hit all segments, but for Upscale Casual they may be curbing visit frequency at higher price points. Even higher-income guests, who are holding up better overall, may be trading down on some occasions as a tougher outlook dominates the narrative.

Meanwhile, Casual Dining is aggressively pressing its value advantage and stealing share. Upscale Casual guests are prime trade-down targets; when Casual Dining delivers a solid experience at a meaningfully lower price, it becomes harder to justify paying more as the economy cools and consumers feel the pinch.

Staffing, Workforce, And Employment Focus

Current Turnover Trends in Full Service Restaurants

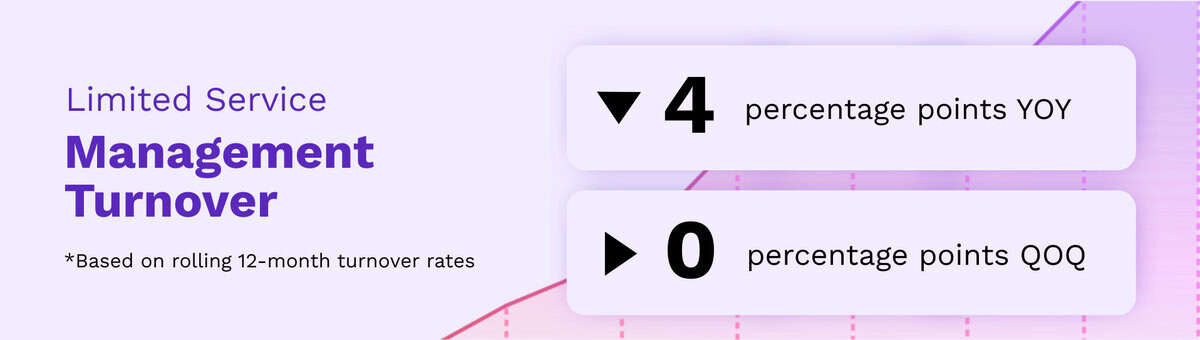

Management turnover in Limited Service has steadily eased for years, rebounding from the pandemic shock—and it now sits two percentage points below 2019 levels. But the decline appears to be stalling: in Q3 2025, turnover was a sizable four percentage points lower than a year ago, yet showed little to no quarter-over-quarter movement once rounded.

The macro backdrop could nudge turnover lower again. The labor market is softening rapidly, with unemployment rising fastest among workers 24 and under—the very cohort Limited Service brands rely on for employees and many managers. More slack means more staff stay put.

Higher unemployment can help Limited Service in two ways. First, retention—especially of managers—moves the needle. Black Box Intelligence data shows locations that kept their General Manager for the past 12 months delivered, on average, same-store traffic two percentage points stronger than units that experienced GM turnover, and they retained the rest of the team better as well. Second, when the economy tightens, consumers trade down more dining occasions to lower-priced options, and Limited Service segments typically capture that shift.

Our Take on State of the Restaurant Industry in September 2025

BBI Says…

“Consumer resilience looks tapped out, and spending is starting to pull back. Same-store sales peaked in the third week of September and have trended down since; the first week of October shows more of the same.

“That slide isn’t shocking. What was surprising was how strong sales stayed in recent months despite an economy shedding jobs, unemployment and inflation edging higher, and consumers growing more worried about price increases over the next year.

“Expect Q4 2025 to bring further weakening in same-store sales and traffic. Looking ahead, 2026—especially the first half—doesn’t set up for strong restaurant growth either.

“Amid this backdrop, Quick Service and Fast Casual reclaimed top-tier status in Q3, trailing only Casual Dining (a notable outlier this year). History and current data align: in periods of economic stress and high inflation, Limited Service brands outperform. With value perceptions guiding choices—and affordability rising in importance—Quick Service and Fast Casual remain best positioned for the months ahead.”

State of Restaurant Industry

Quarterly Webinar Deepdives

We go into way more detail in our flagship quarterly State of the Industry (SOTI) webinar – our definitive take on the latest developments and a must attend for anyone in the restaurant industry.